March 7, 2025

Omnibus Proposal (Part 2)Simplified regulation strengthens competitiveness

No matter how ESG regulations evolve, our proven, specialized solutions support you with your reporting. With software and services, integrated for both non-financial and financial reporting. Automate and simplify your processes and communicate your achievements to stakeholders in professionally designed reports in PDF, online HTML, and/or XBRL format.

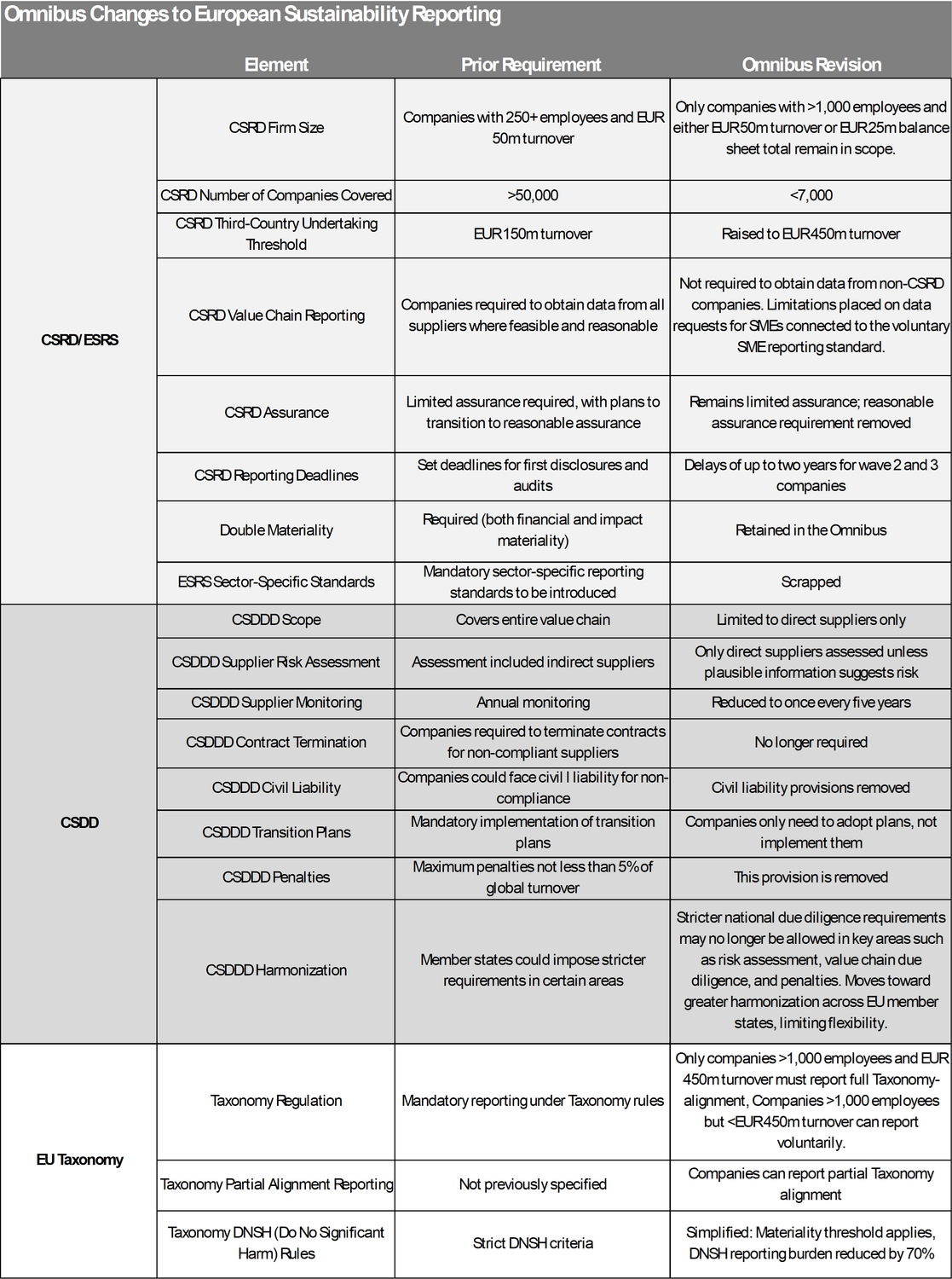

Recently, the EU introduced significant changes in ESG reporting. Under the term “Omnibus Packages,” key developments are proposed that, in particular, massively reduce the number of companies affected by the regulations and the extent of data points to be reported.

The first Omnibus package aims to strengthen competitiveness in the EU and support the Green Deal. The key goals: less complexity, more efficiency, and a stronger focus on investments and sustainability measures instead of bureaucracy.

Currently, the Omnibus simplification package is a proposal from the EU Commission, which will next be debated by the European Parliament and Council in Q2/2025, with approval expected by the end of 2025. However, some countries, such as France, Italy, and Sweden, have already implemented the original requirements into national law and are concerned about the legal uncertainty, potential costs of adjustments, and the risk of undermining the credibility of EU sustainability efforts.

Key proposed adjustments

The main changes in sustainability reporting concern the scope of affected companies, timeframes, and the extent of data points.

Thresholds

- CSRD (Corporate Sustainability Reporting Directive): Reporting obligations apply only to large companies with more than 1,000 employees and either a turnover exceeding 50 million euros or a balance sheet total exceeding 25 million euros.

- CSDDD (Corporate Sustainability Due Diligence Directive): Comprehensive due diligence obligations will only apply to large companies with more than 1,000 employees. All other companies will be exempt from direct due diligence obligations. Additionally, only the company’s own activities, those of its subsidiaries, and direct business partners need to be evaluated, excluding indirect business partners.

- EU Taxonomy: Large companies with more than 1,000 employees and a turnover of more than 450 million euros are required to report under Article 8 of the Taxonomy Regulation. Large companies with more than 1,000 employees and a turnover between 51 and 449 million euros can report voluntarily.

Key Takeaways

- Reduced scope: The number of affected companies will be reduced by about 80%.

- Cost savings: The proposed measures to reduce the scope of CSRD and reporting obligations for companies within scope, along with future changes to the ESRS, will generate significant cost savings for companies.

- Time shift: Timing remains the same for companies with more than 1,000 employees. For all other companies, CSRD reporting obligations are postponed by two years. (Under the current CSRD, this applies to companies under Wave 2 = market-listed companies with over 250 employees that must report starting in the 2026 financial year, and Wave 3 = market-listed SMEs, which must report from the 2028 financial year). The CSDDD deadline is delayed by one year to July 2028.

- Revision of ESRS (European Sustainability Reporting Standard): The scope of data points will be significantly reduced, and unclear provisions will be clarified.

- Abolition of sector-specific standards: These will be completely eliminated.

- Simplification of EU Taxonomy: Reporting templates will be simplified, and the scope of data points will be reduced by 70%.

- SMEs: Small and medium-sized enterprises will be protected from extensive reporting obligations.

- Voluntary Reporting: Companies outside the scope can voluntarily report using a simplified standard.

Additionally, the Omnibus package proposes relief for the CBAM (Carbon Border Adjustment Mechanism): The pricing of CO2 emissions from imported goods aims to prevent carbon leakage.

The simplification introduces a minimum threshold of 50 tons per year, which exempts 90% of importers from reporting obligations.

Summary

The goal is to significantly reduce administrative burdens, promote investments, and increase the competitiveness of EU companies. The following graphic shows the specific simplifications in a practical overview.

Detailed information on all proposed changes is available in the EU Commission's Q&A document:

EU Commission Q&A

Impacts for Companies

The Omnibus initiative has sparked discussions about changes to the CSRD and ESRS simplifications, and now many companies are asking what the next steps are. Now is the time to shift the feared effort to meet regulatory requirements and show initiative.

Why is this important? The proposed simplifications create room for action to unlock new value creation potential through investments in environmentally and socially sustainable products and services. A clearly sustainability-focused strategy can not only help differentiate from competitors but also secure long-term competitive advantages. Companies that act now and embrace sustainability as the core of their strategy are in the best position to emerge as winners in this transformation. ESG reporting will become a champion of achievements, rather than just a compliance report.

Stand out with your (voluntary) sustainability reporting

With our platforms, we help you not only efficiently and automatically create your ESG report but also present it professionally for stakeholder engagement and dialogue with your stakeholders across all desired channels. This, by the way, is independent of how the regulations evolve. For every standard, whether ESRS, GRI, or ISSB. Including machine readability.

For non-listed SMEs, the newly introduced VSME Standard (Voluntary Sustainability Reporting Standard for non-listed micro, small, and medium enterprises) provides a practical solution. It offers a structured approach to disclose sustainability data clearly and consistently, meeting the growing market demands from investors, banks, and business partners. It also serves as good preparation for potential future ESRS reporting obligations.

Personal Consultation

Are you also driven by the Omnibus package? Do you see your potential? Are you wondering how to absorb the high dynamics of change in your reporting project? Would you like to report your sustainability achievements in a beautiful ESG report – beyond technical standards? The specialized platforms ns.wow and ns.publish ensure security, simplify, and empower you in your sustainability communication – also possible as an integrated project with financial reporting, including ESEF/XBRL.

Our experts, Olivier Neidhart and Daniel Schön, are happy to answer your questions. Book a meeting directly: